This post is not sponsored by the banking companies mentioned in this article.

Why get an ATM card for international travel?

When traveling internationally, having cash, and more importantly – having access to cash is critical. One additional way you can save money during your trip is by getting an ATM card with no international fees and no ATM withdrawal fees (reimbursed). While you could buy foreign currency from your local bank and bring that with you on your trip, having these fee-free ATM cards is more ideal because:

- You don’t have to travel with a large amount of cash (not safe)

- If you’re away from your hotel and need more cash, you can swing by the nearest ATM

- Better rates than currency exchange

- You can get small bills by doing multiple transactions at no additional cost

The ATM withdrawal fee varies upon country and bank – the highest I’ve seen is in Singapore, where one bank charges 8 SGD (~$6 USD) per withdrawal.

I have 2 ATM cards that reimburse the ATM withdrawal fees. The ATM fee is charged by the ATM operator when you are doing the withdrawal, but gets reimbursed at the end of the month. Do make sure you have enough money in your accounts to front the ATM fees before they are reimbursed.

I do not use these for international transactions (such as paying for things at the store, restaurants, etc), only withdrawing from ATMs.

If you are not a US resident, you may need to search for a card issued in your country. Be sure to look for the same things: no international transaction fees, no ATM withdrawal fees, fraud protection, ability to lock/unlock card, and no service fees.

The two that I use are:

*Please read through all the updated information on each bank website before opening an account and using the debit card as terms and conditions are subject to change.

Charles Schwab – Visa Platinum Debit Card

(by opening a Schwab Bank Investor Checking Account).

Full details here: https://www.schwab.com/checking/debit-card with additional FAQs here: https://www.schwab.com/checking/faqs

This benefits of this card:

- No balance minimum or service fees

- No foreign transaction fees

- ATM Fee reimbursements

- VISA is also widely accepted internationally so it will work with most ATMs

Thus, you can open and use this account only for travel, if you wish.

Fidelity – Cash Management Account

The Fidelity cash management debit card offers the same ATM fee reimbursements and no foreign transaction fees as Charles Schwab does.

Make sure that the debit card is for the Cash Management Account. Certain Fidelity cash accounts are eligible for a debit card, but do not reimburse ATM fees!

Full details here: https://www.fidelity.com/spend-save/atm-debit-card

Betterment

Another debit card offering reimbursed ATM fees + no foreign transaction fees is: Betterment (though I personally do not have this card).

Full details here: https://www.betterment.com/checking

Fraud Monitoring

As ATM cards are technically debit cards and are still vulnerable to fraud, I suggest having more than one ATM card so that you always have access to cash in case you need to freeze and re-issue the card if fraud has occurred. If you get both the Charles Schwab Visa Platinum Debit Card and the Fidelity Cash Management Account ATM card, both are able to be locked via the app.

Be sure to enable transaction notifications so you can monitor withdrawals and report any suspicious activity. You can also set international travel notices so your legitimate withdrawals don’t get blocked.

Tip for getting small bills

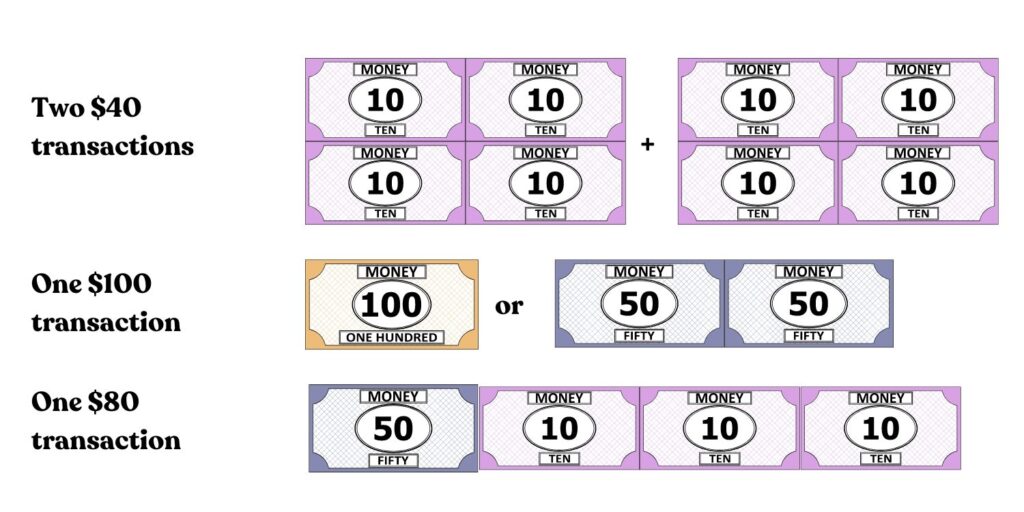

One other thing that is super useful with having no withdrawal fees is that you can do multiple transactions in order to get small bills. You should do research on your destination country’s currency in order to figure out the best amounts to withdraw.

Let’s say I am traveling to Singapore. At the ATMs, you are only able to withdraw in increments of $10, and only $10 or $50 bills are given. I do not like getting big bills (in this case, $50) in case vendors don’t want to accept it to give change.

However, because all my ATM fees are going to be reimbursed, I can do multiple transactions even if I need more than $50. Therefore, I am going to split my transactions into 2: in one transaction I will withdraw $40. Once that transaction is completed, I will start another transaction where I will also withdraw $40.

I will then receive 4 $10 bills per transaction. If I tried to withdraw $100, I would likely get two $50 bills or one $100 bill. Or if I did $80 in one transaction, I would probably receive 1 $50 and 3 $10 bills.

Additional money saving tips

Because there are no international transaction fees with the cards I listed, no matter what country you are, ALWAYS withdraw at the LOCAL currency rate. The ATM will ask you if you want to charge your bank account using USD or local currency (this is known as “Dynamic Currency Conversion”).

If you select local currency, the amount will automatically be converted to USD based on the exchange rate at the time the transaction occurs (the same way foreign transaction conversions occur on credit card transactions). The USD option always has a markup. The additional markup will be not reimbursed by either of the cards above.

Be sure to leave ample time to open an account, transfer money to your account, and receive the debit card in the mail before your international trip.

You can also set Travel Notices up on your debit cards so your transactions don’t get blocked while trying to withdraw money during traveling when it’s legitimately you.

The same can be applied for credit cards – when traveling internationally (or even purchasing online from non-US sellers), make sure you bring multiple credit cards that charge no international transaction fees. Want to know which one I use for travel? Check out my post above!

Related

The only travel credit card you need: Capital One Venture X

The only travel credit card you need: Capital One Venture X

Ultimate Singapore Travel Guide: Everything you need to know

Ultimate Singapore Travel Guide: Everything you need to know

Ultimate Seoul Travel Guide: Everything you need to know

Ultimate Seoul Travel Guide: Everything you need to know

Seoul: Guide to Solo Dining / Eating Alone / 혼밥 Honbap

Seoul: Guide to Solo Dining / Eating Alone / 혼밥 Honbap

How to use Naver Maps in English for directions and finding menus

How to use Naver Maps in English for directions and finding menus

Hong Kong Airport: Plaza Premium Lounge – Review

Hong Kong Airport: Plaza Premium Lounge – Review